The U.S. dollar, as measured by the DXY index, rebounded moderately on Tuesday after suffering its biggest daily drop in nearly two months at the beginning of the week. In afternoon trading in New York, the greenback’s gauge was up about 0.3% to 104.75, threatening to return to multi-month highs just as sentiment started to sour.

The dollar's gains were driven partly by rising oil prices. Early in the day, WTI futures rallied more than 2%, breaking above the $89.00 threshold and reaching their highest level since November 2022. Higher energy costs could keep the Federal Reserve on its toes, ensuring that monetary policy remains restrictive for an extended period to force inflation down to the target in a sustainable manner.

Elsewhere, the Nasdaq 100 fell more than 0.75% to 15,350, reversing part of its advance from the previous session, dragged down by a pullback in technology stocks, which have rallied strongly in recent months and currently command lofty valuations despite numerous macroeconomic headwinds.

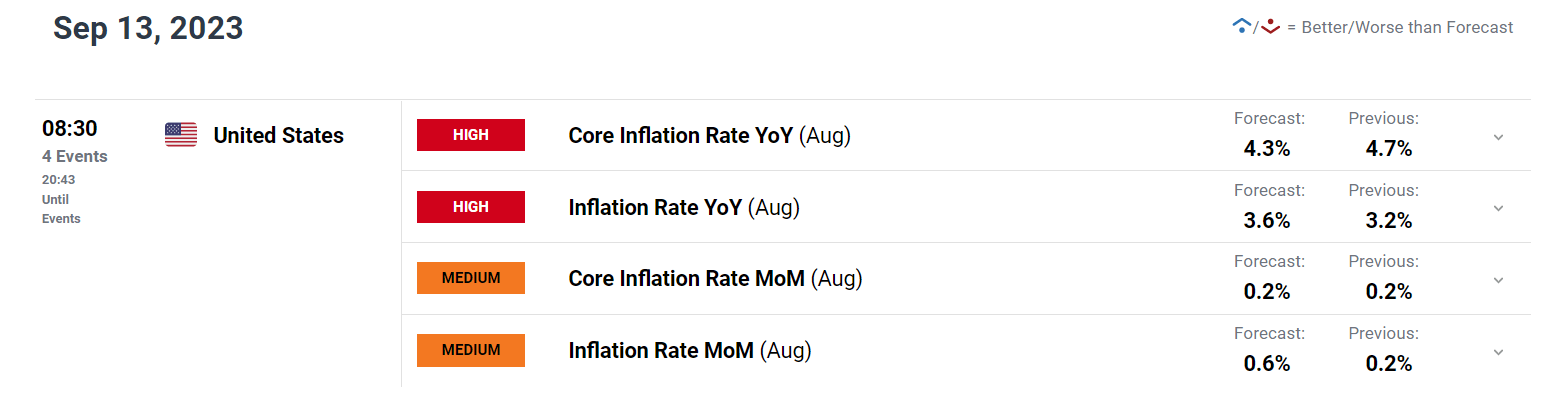

Focusing on inflation, a clearer picture of the broader trend in consumer prices will emerge on Wednesday when the U.S. Bureau of Labor Statistics releases data from last month. This event holds considerable significance, as it could inject volatility into the financial markets and offer crucial insights into the short-term trajectory of major assets.

In terms of Wall Street’s projections, headline CPI is forecast to have risen 0.2% m-o-m in August, with the annual rate accelerating to 3.6% from 3.2% previously. Meanwhile, the core indicator, which excludes food and energy, is seen climbing 0.2% m-o-m, resulting in a 12-month reading of 4.3%, down from July's 4.7%, a welcome development for the U.S. central bank.

UPCOMING US DATA

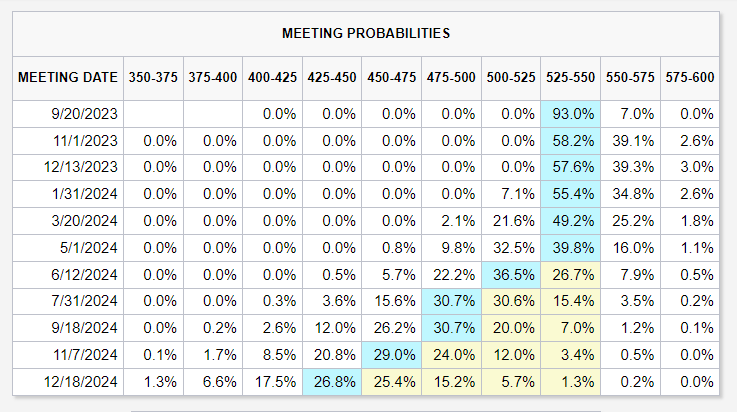

The Fed has embraced a data-centric stance and noted that it will “proceed carefully” after having already delivered 525 basis points of tightening since the start of the normalization cycle. This message has all but eliminated the likelihood of additional policy firming in September, but has left the door open for a quarter-point hike at the November FOMC meeting, with the probability of the latter event at ~40% (see table below).

FOMC MEETING PROBABILITIES

Source: FedWatch Tool CME

Given the Fed’s high sensitivity to incoming information, traders should carefully watch the CPI report, paying particular attention to underlying trend dynamics. That said, any upward deviation in the official data from consensus estimates could boost the U.S. dollar and undermine the Nasdaq 100 by pushing interest rate expectations in a more hawkish direction and reinforcing the case for “higher-for-longer”.

Conversely, in the event of muted inflationary pressures, the reverse scenario holds true. If the results for August inflation fall substantially below expectations, market participants might take action to unwind any remaining bets on further rate hikes in 2023, sending the greenback lower across the board and boosting the Nasdaq 100.

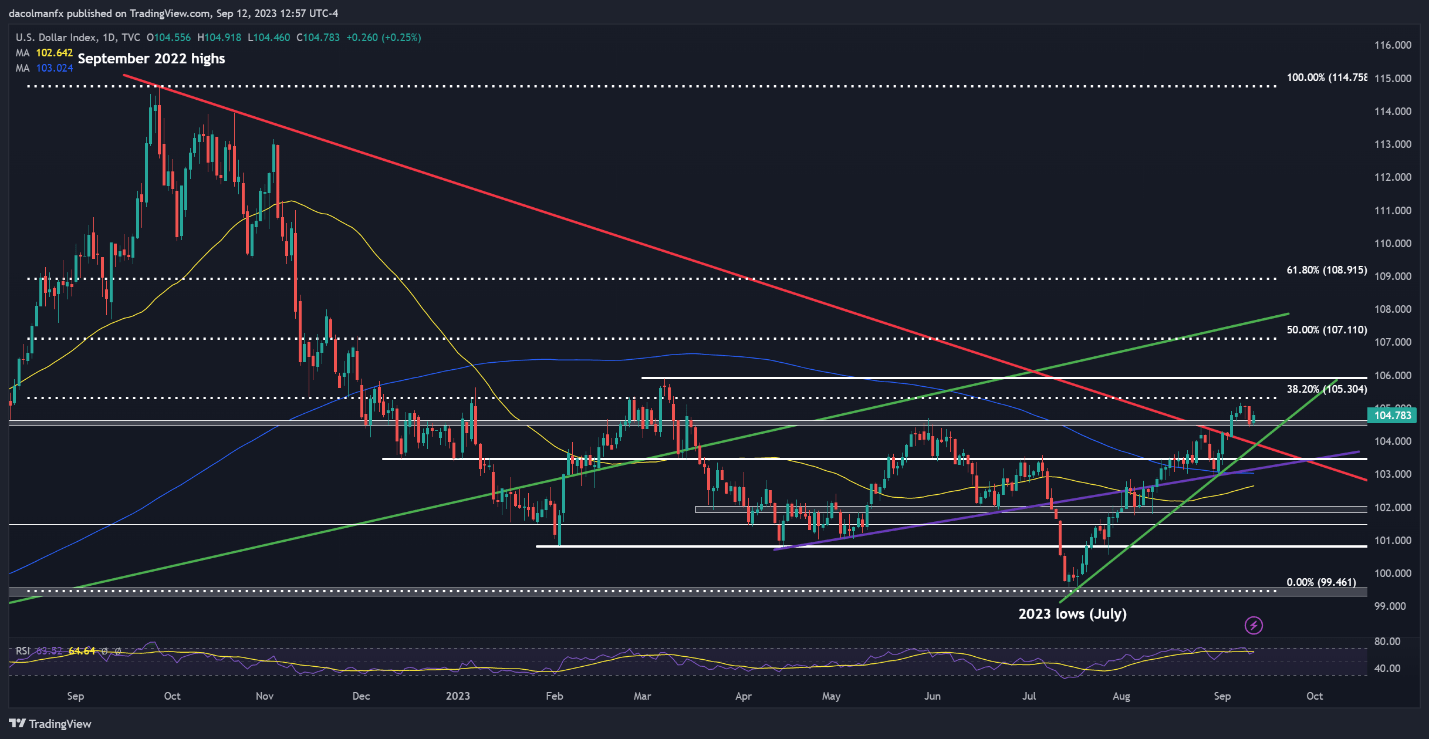

US DOLLAR INDEX (DXY) TECHNICAL ANALYSIS

The U.S. dollar broke out on the topside last week, breaching trendline resistance and besting its May peak decisively, before briefly setting a fresh multi-month high above the 105.00 handle.

With bullish momentum clearly dominating the market, the DXY index could sustain its upward trajectory for now, especially if it manages to stay above technical support at 104.50. Under this scenario, we might witness an advance toward 105.30, a noteworthy resistance created by the 38.2% Fibonacci retracement of the Sept 2022/July 2023 slump. Further strength could lead to a retest of the March highs.

On the contrary, if sellers regain control and trigger a retreat, initial support can be found at 104.50, followed by 103.95. On further weakness, the next significant support zone comes in at 103.50.

US DOLLAR (DXY) TECHNICAL CHART